In this

brief overview, I will attempt to demonstrate why it is so important to invest

research into channels outside that of the superstore, where, let’s be honest,

we know quite a lot!! For simplicity, I

am considering discounters by their store type rather than their business

models.

{kind=link}

Superstores

are more and more being seen by shoppers as the channel to avoid if at all

possible “Can I manage without ever going in one?”….”Who wants to trail round a

superstore in their leisure time?”….”I dread the experience”….”We pile our

trolley high with things we probably won’t even eat”….people love eating, but

don’t particular like shopping. How

different this is from our French neighbours whose mission is to find the best

quality food, in the UK it is so much more functional than that. So, what are

the alternatives?

The rise of

the convenience sector, driven by the increasing store estates of the multiples

have given shoppers the wider choice to buy just what they need, when they need

it. This all from retailers they know

and trust (most of the time!), where the biggest brands are still available at

reasonable prices (although they also recognise they are paying for the

privilege, they seem happy to do so).

And convenience really is the key as they combine their commutes with

manageable quantities of product, where the consumption occasion is already

known…”Maybe I spend a bit more, but I know that it’ll all get eaten with no

waste”.

Online

continues to grow at above 20% per year, but from a low base, this is still

pretty small in the whole scheme of things, but our research suggests we are

nearing the tipping point for even faster expansion in this channel. The introduction of click & collect in

the way they have in France (where one can order at work in the afternoon, and

two hours later drive to a designated car park – dark store or store car park -

and have their goods loaded into their Renaults), will revolutionise the online

channel beyond recognition. No longer

will waiting at home for a two hour slot be seen as convenient, and if they

forget to order something, they can still nip into the store to augment their

online order at the same time.

I also

predict a dramatic rise in shoppers using non-standard grocery channels such as

Amazon, where they benefit from big discounts on non-perishable produce, and

larger SKU’s which they don’t mind storing if the price is right. Manufacturers will ignore this at their cost,

with the opportunity to sell SKU’s that superstores will not stock, there

should be no issues. I believe shoppers

will change their mind-sets on where to buy certain products, fresh is one

thing…but boxes of their favourite brands is another, and anyway they already

have an account!

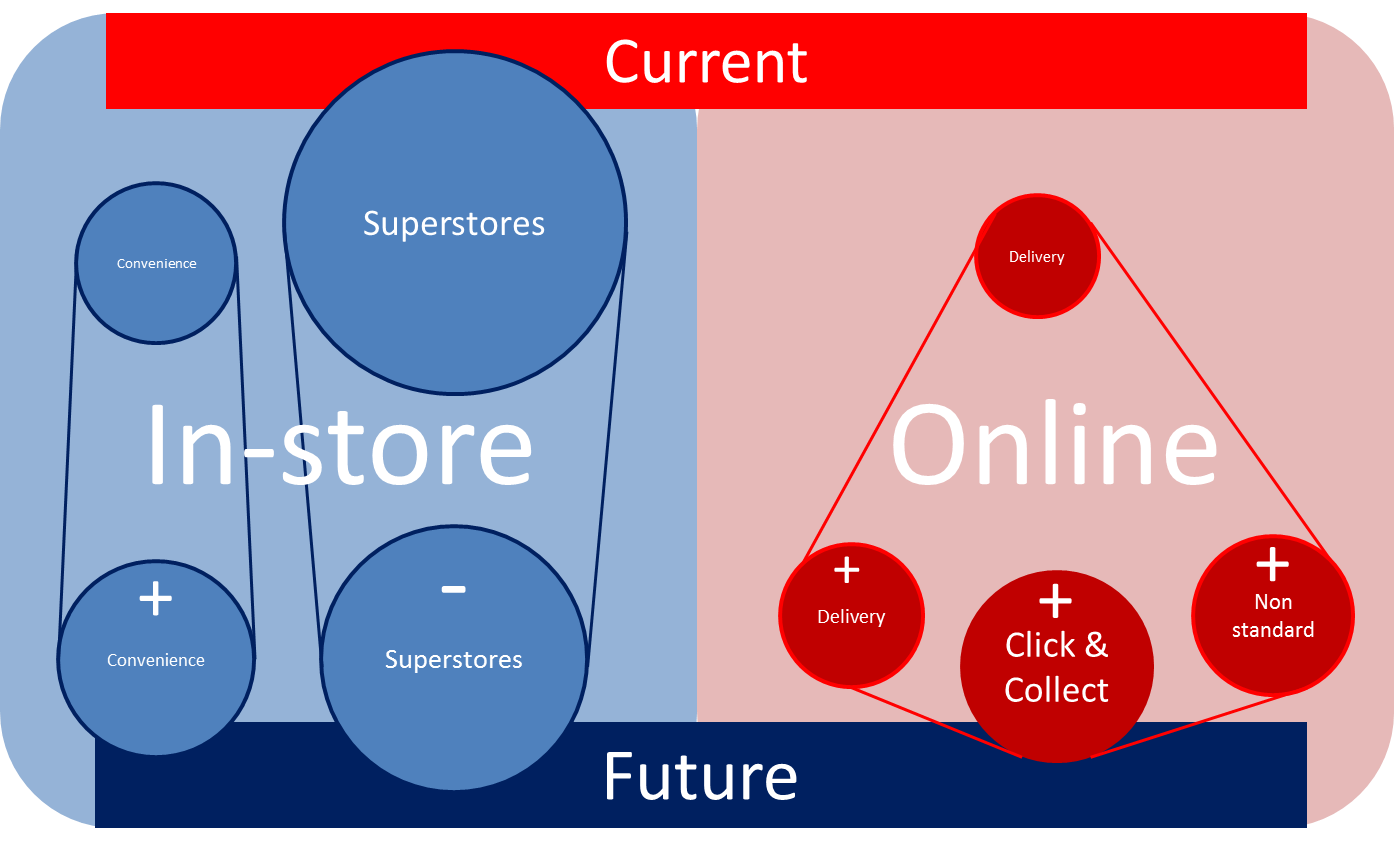

So in

summary, the market will demand less supermarkets, continuing growth in the

convenience sector, whilst online will establish itself as the key channel for

larger shopping missions with a shift to more click & collect methodology

and the growth of non-standard grocery channels (like Amazon).

{kind=link}

No comments:

Post a Comment